Given recent economic turmoil, three things are likely to characterize the city’s job market for the next year or two

COVID-19 Economic Update is a bi-weekly column prepared by economist James Parrott of the Center for New York City Affairs (CNYCA) at The New School, whose research is supported by the Consortium for Worker Education and the 21st Century ILGWU Heritage Fund. Read past installments here.

The economic news of late has been much like the weather this spring—some days are sunny with balmy temperatures while on other days it’s unseasonably chilly and pouring rain for hours on end. However, what lies ahead is not as certain as the likelihood of a lot of heat and humidity as spring turns to summer.

At the end of April we heard that first quarter Gross Domestic Product fell but last Friday’s report on the national jobs picture for April showed another month of strong job gains with the unemployment rate holding at 3.6 percent, one of the lowest levels over the past half-century. Inflation is running at its highest level in forty years and to dampen that inflation, last week the Federal Reserve raised the key interest rate it controls by a half-percentage point, the largest increase in twenty years. Then there’s the stock market gyrations with the largest up and down movements in two years occurring on consecutive days last week as investors try to make sense of this jumbled Covid-affected recovery that is complicated by Russia’s murderous assault on Ukraine.

What do these various cross currents mean for the New York City’s struggling job market? In my opinion, three things will characterize the city’s job market for the next year or two.

- New York City’s job recovery will remain incomplete (i.e., below pre-pandemic employment levels) well into 2023 and possibly 2024;

- Federal Reserve actions to curb inflation will almost certainly slow the economy and could bring on a recession; and

- Black, Latinx, less-educated, and young workers will bear the brunt of high unemployment that will erode incomes for many low-income families, possibly reversing the significant progress made in the five years before the pandemic.

First, let’s talk about the new issue on the block—inflation. There has been considerable debate about the factors driving the current high inflation. The commonly cited explanation is that historic levels of federal government Covid-related spending “over-heated” consumer demand and that rising wages and pandemic-related supply chain bottlenecks have pushed up prices. However, there is also a view, recently articulated by Economic Policy Institute economist Josh Bivens, that increased corporate profit margins have contributed over half (54 percent) of the increase in prices, and that labor costs account for only eight percent of the increase. Nonlabor input costs, e.g., shipping costs, affected by pandemic bottlenecks—account for the other 38 percent.

Bivens notes that the typical pattern prior to the 2008-09 Great Recession had the labor share of income rising and the corporate share declining as unemployment fell in a recovery. In the first six quarters of the pandemic recovery, however, the labor share of income fell. Bivens notes that the recent rise in corporate profits isn’t because there has been a pandemic-era increase in corporate power, but rather, that corporations were not able to suppress wages as occurred in the recovery from the Great Recession. Pandemic-affected turbulence in the job market led employers of all sizes to increase wages to attract workers, but still, wage increases have not kept up with price increases. In recent months, many corporations have touted on earnings calls with large investors their ability to bolster profits by raising prices.

The Federal Reserve’s pushing interest rates higher will cool consumer demand, but at the expense of higher unemployment and weaker wage growth. Biven’s suggestion for a temporary excess profits tax warrants consideration, but that is unlikely given the current political situation.

While the nation is within a couple of months of returning to its pre-pandemic employment level, New York City’s March job total was only back to about 75 percent of the pre-Covid level. There is likely to be some degree of residual job shortfall for several more months in some of the hardest-hit leisure and hospitality industries. There hasn’t been much growth in recent months in the remote-working set of industries (mainly finance, information, and professional services), and job growth in those sectors usually weakens when the national economy slows or enters a recession. The city usually also sees a decline in high-paying jobs spill over into local service jobs, where many industries are still far from having recovered from Covid-related shutdowns.

On the other hand, while Amazon reports that it will rein in investments in new warehouse capacity, hiring will likely continue when it opens two New York City facilities that are nearing completing. Recent state budget actions affecting home health care and child care jobs should support higher pay for those traditionally-underpaid female-dominated sectors, and should result in increased employment opportunities. Increased hiring of child care workers, however, may be several months in the future since much work remains to be done to flesh out how that expansion will occur.

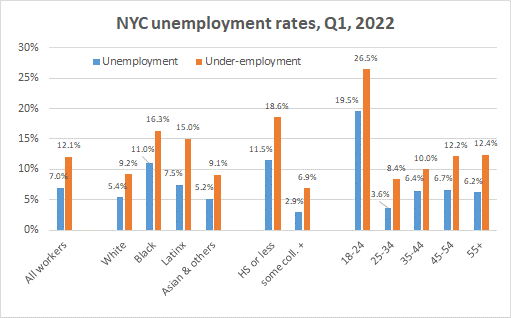

Unemployment has come down from sky-high levels two years ago but it is still much higher than the national rate. For the first quarter of 2022, New York City’s seasonally adjusted unemployment rate was 7.0 percent compared to 3.8 percent for the nation overall. However, as we know all too well, unemployment rates vary considerably by race and ethnicity. While the first quarter unemployment for white city residents was 5.4 percent, it was more than twice that (11.0 percent) for Blacks and 7.5 percent for Latinx workers. Wide disparities exist also when considering the under-employment rate that factors in discouraged workers and involuntary part-time employment. The under-employment rate for Blacks was 16.3 percent in the first quarter and 15 percent for Latinx workers. Unemployment and under-employment rates for Asian and other workers are similar to the rates for whites.

As we have seen all along over the past two years, unemployment has hit hardest at less-educated and younger workers. First quarter unemployment for those with a high school education or less was 11.5 percent, and under-employment was 18.6 percent. For young adults ages 18-24, unemployment in the first quarter was nearly 20 percent (19.5) and more than one out of every four young adults (26.5 percent) experienced some form of under-employment.

The Federal Reserve’s actions to slow the economy almost certainly means continued high unemployment for the Black, Latinx, less-educated, and young workers. And this will likely result in low earnings and little prospect for income growth to keep up with inflation. As we documented in our recent report on the twin economic challenges facing New York City in emerging from the pandemic, full employment coupled with rising labor standards can make a powerful difference in broad measures of economic improvement. Given recent developments, the city’s recovery could be on the verge of being stalled indefinitely.

Local policy makers have little say over how the country chooses to rein in inflation, but they can ensure that care workers and under-compensated human service contract workers receive higher pay, that the state’s minimum wage is finally adjusted for the rising cost of living, that job quality is improved for gig and other low-paid independent contractors, and that young workers of color are trained for family-sustaining jobs in tech, health care, and other fields.

# # #